Last updated on July 14, 2025

Artificial Intelligence (AI) has moved from theoretical promise to real-world application at a pace unlike any other technology in modern history. In 2025, AI is not just another frontier, it is the infrastructure of the present and the blueprint of the future. Once the domain of specialised researchers and experimental labs, AI is now embedded into everything from consumer services and industrial operations to national defence and scientific discovery.

According to the Tech Nation UK AI Sector Spotlight, 3 in 4 UK tech leaders say AI is having a positive impact on their company’s growth; 1 in 2 have improved their products and services as a result of AI.

These trends are repeated globally. Over 73% of organisations worldwide are either using or piloting AI in core functions. Meanwhile, public trust in AI is evolving: 56% of global citizens now believe that AI will positively transform their lives in the next 10 years, although 68% also support increased regulation of AI systems. (Source: TechNation)

This white paper is designed to be a comprehensive guide to the current state and future direction of AI globally. It is structured to provide insights and data for multiple stakeholders—startup founders, policymakers, investors, enterprise leaders, academics, and the broader public.

Drawing on trusted sources including Tech Nation, Exploding Topics, the OECD, Stanford HAI, and global VC data platforms, we provide a 360-degree view of the AI landscape as it stands in 2024–2025—and where it is likely headed by 2030.

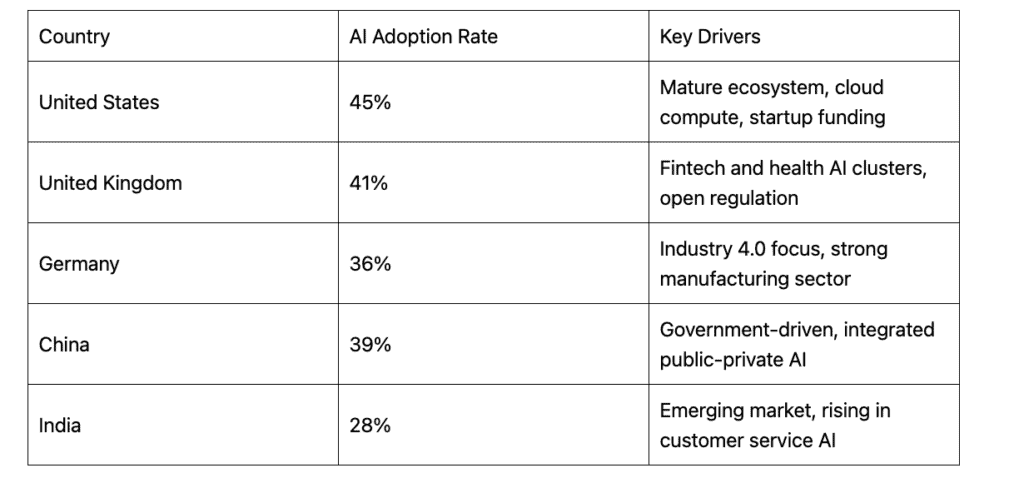

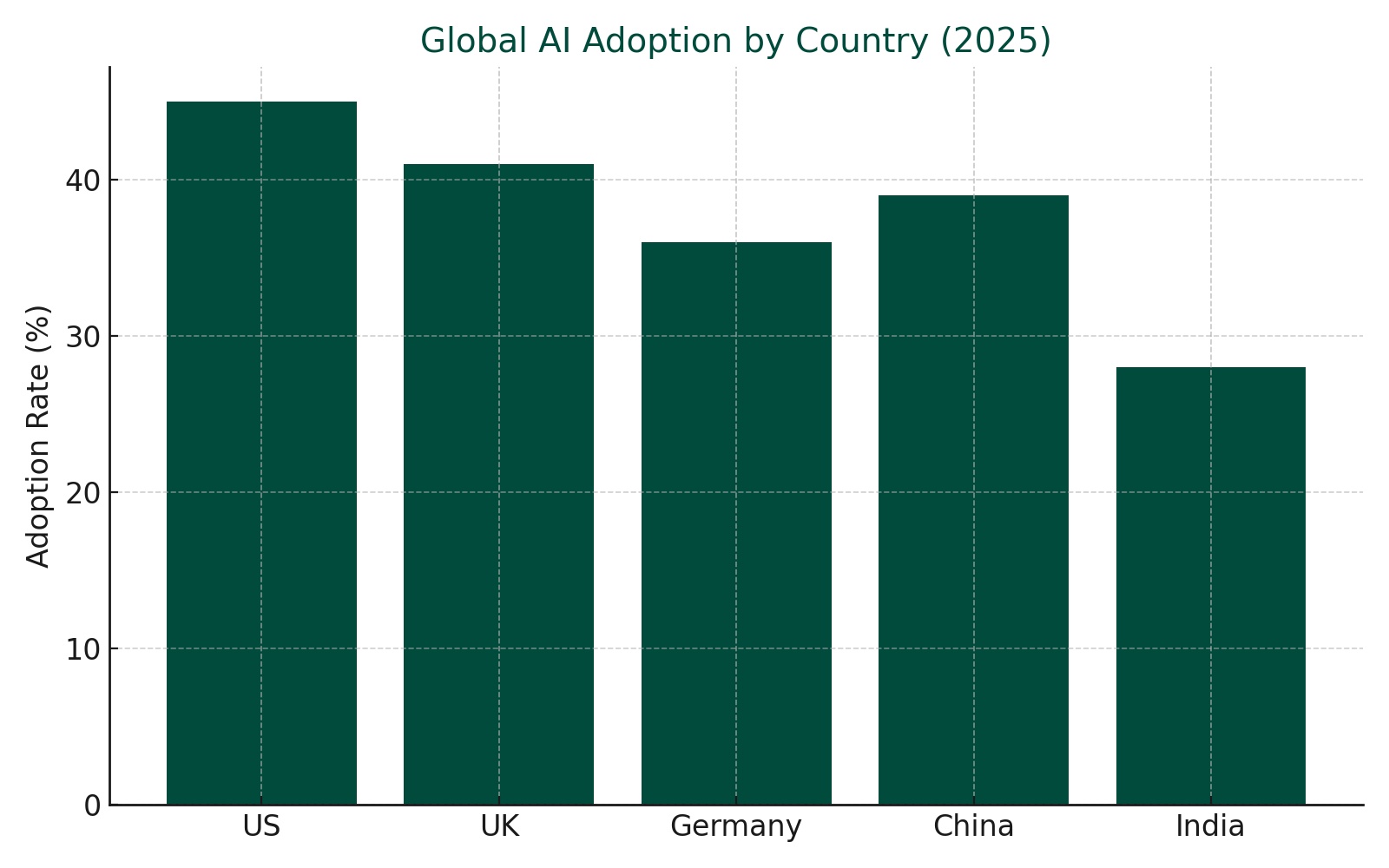

Global AI Adoption Rates (2025)

AI adoption across sectors and geographies is accelerating quickly, but not uniformly. In 2025, adoption is defined by three forces:

- Access to infrastructure (compute, talent, and data)

- Strategic prioritisation by leadership

- Regulatory readiness and public trust

Global Snapshot

According to Exploding Topics:

- 35% of businesses have fully deployed AI in at least one function.

- 42% are actively experimenting or piloting AI tools.

- Just 13% have no AI adoption plans.

This means that nearly four out of five organisations are engaging with AI in some form—a historic high.

Country Comparisons

In the UK, the number of active AI companies has grown over 600% in the past decade—from fewer than 250 in 2014 to over 1,400 by 2024. Many of these are based in London, Cambridge, Bristol, and Edinburgh—each forming distinct regional clusters focused on AI safety, NLP, and deep learning. (Source: ExplodingInsights)

Enterprise vs SME Adoption

Large enterprises are more likely to deploy AI across multiple departments—typically using a mix of internal teams, cloud AI platforms (e.g. Google Vertex AI, AWS Bedrock), and third-party tools.

SMEs, by contrast, tend to use off-the-shelf AI capabilities, such as:

- ChatGPT Enterprise

- Canva’s AI design assistant

- HubSpot’s AI-powered CRM tools

- Jasper for marketing content generation

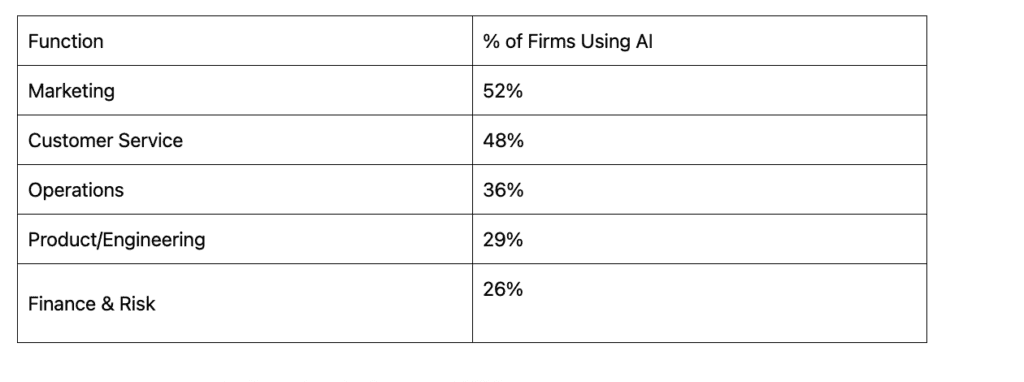

Use Case Distribution

Enterprises in the top quartile of AI maturity report 15–30% improvements in productivity, retention, and customer satisfaction across AI-enabled workflows.

Talent Distribution

AI talent remains highly concentrated. According to LinkedIn data:

- The United States and India account for over 50% of the global AI workforce.

- The UK ranks third globally for AI talent density per capita.

- Cities such as Toronto, Tel Aviv, Berlin, and Singapore are also emerging as high-talent-density AI clusters.

Infrastructure Access

AI adoption requires significant compute capacity. Many countries are launching national compute strategies, such as:

- UK’s AI Research Resource (AIRR) – aims to boost sovereign compute

- France’s GENCI initiative – public HPC for AI

- Singapore’s National AI Office – linked to their cloud-first policy

These infrastructure efforts will determine whether nations can scale AI from experimentation to deployment.

3. AI Market Size & Growth Forecast

The global artificial intelligence market is entering a period of exponential growth. As of 2025, it is valued at $391 billion and projected to reach $1.81 trillion by 2030. This expansion is driven by increasing enterprise adoption, rising consumer AI interactions, and public-sector integration.

Global Market CAGR: 35.9% (2025–2030)

This rate is faster than the cloud computing boom of the 2010s and the mobile app economy of the early 2010s.

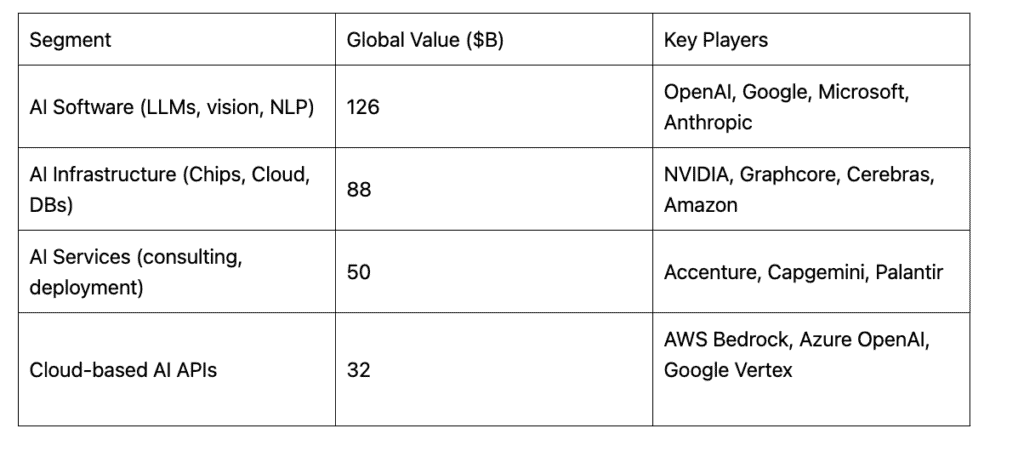

Market Segmentation (2025)

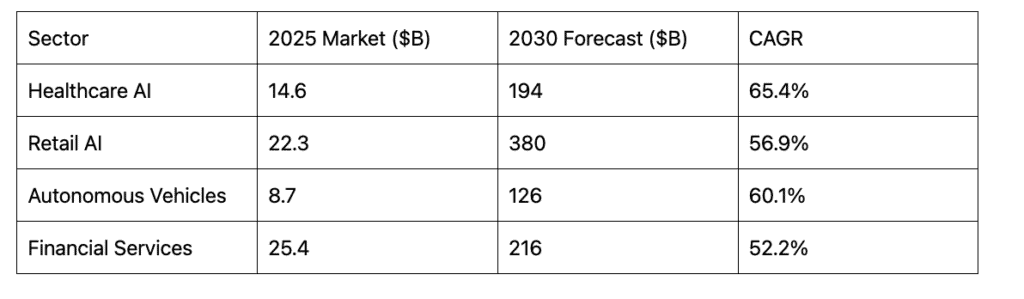

Sector Growth Forecasts

Regional Investment Trends

- US: Continues to dominate foundational AI model development and private investment volume

- UK: Europe’s AI investment leader, focused on practical deployment and safety infrastructure

- China: Focused on sovereign models, vertical integration (e.g. SenseTime, iFLYTEK)

- India: Scaling AI for low-resource environments in public health and education

Competitive Landscape

The AI market is seeing an evolving competitive dynamic between:

- Open vs closed models (e.g. Meta’s LLaMA vs OpenAI’s GPT-4)

- Startups vs incumbents (e.g. Mistral vs Google DeepMind)

- Horizontal vs vertical AI (e.g. GPT-4 for everything vs Harvey for legal AI)

Emerging Market Signals

- AI is becoming a required layer in SaaS platforms—over 60% of enterprise SaaS products now have embedded AI features

- Companies are investing in AI “copilots” across departments: marketing, finance, legal, HR

- AI-native apps are emerging in productivity, health, finance, and entertainment—creating an entirely new software category

4. Generative AI: Use Cases & Growth

Few technologies in modern history have matched the growth velocity of Generative AI. From its inception in 2022 with early large language models (LLMs) like ChatGPT and DALL·E 2, to its widespread integration in 2024–2025, generative AI has upended expectations for productivity, creativity, and user experience.

Generative AI User Base & Scale

- 100M+ monthly active users on ChatGPT by early 2023

- 4 billion+ prompts are issued daily across major LLM platforms (OpenAI, Claude, Gemini, Mistral)

- Over 300 enterprise tools have embedded generative AI via APIs or in-product copilots

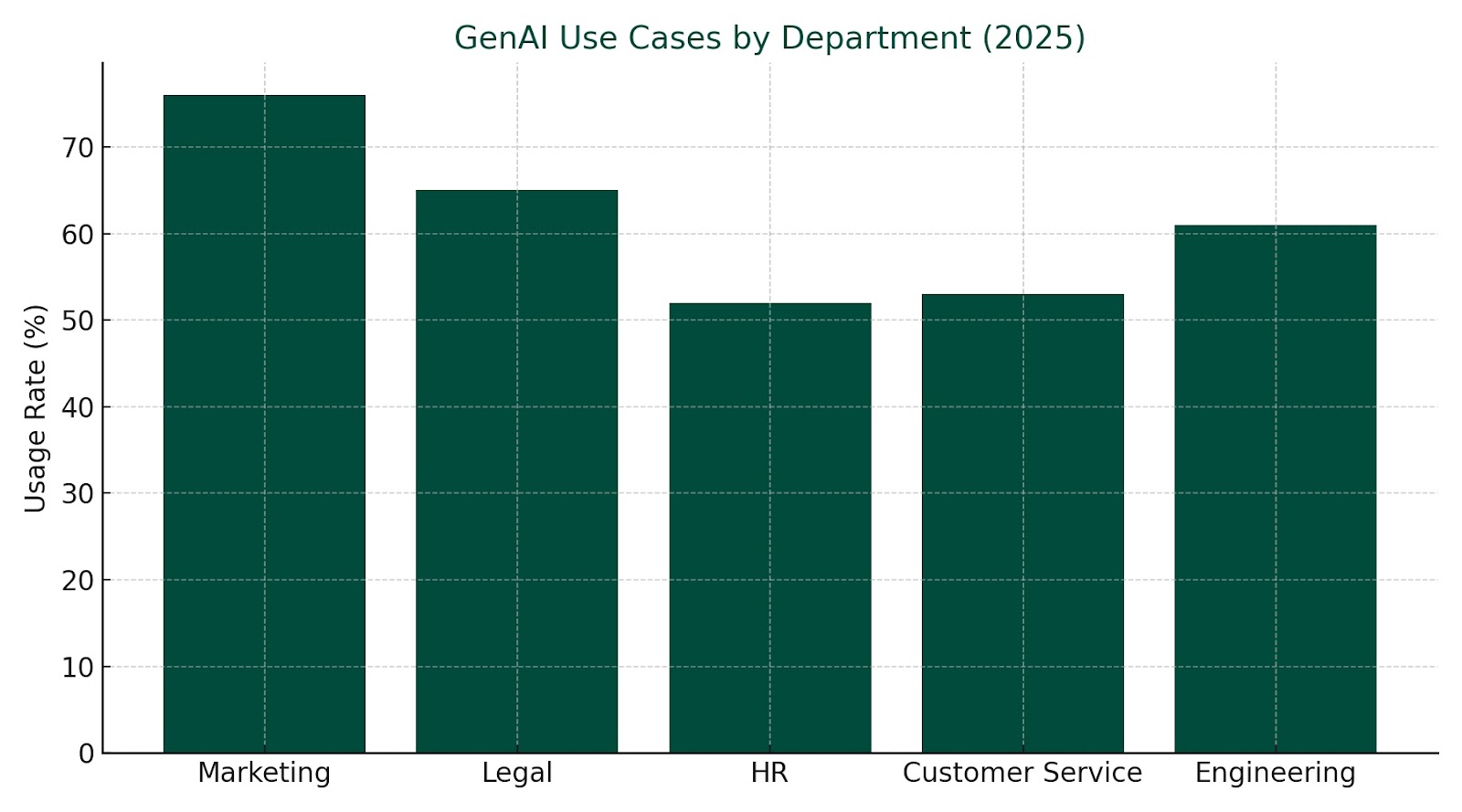

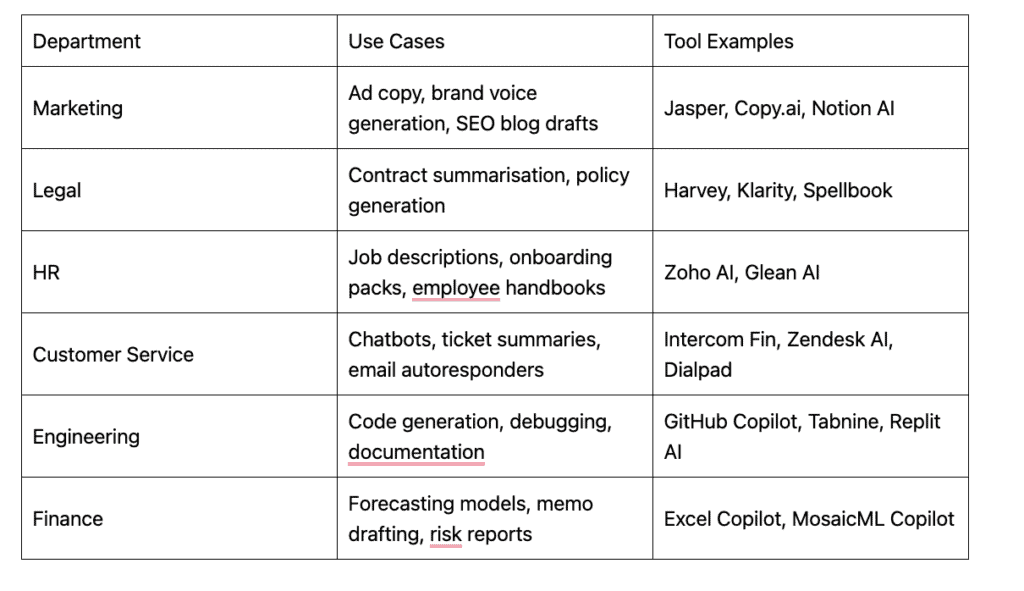

Most Common Use Cases

Real-World Case Studies

- Klarna: Reduced customer support volume by 66% using an AI assistant

- Morgan Stanley: Uses OpenAI’s GPT-4 to power a knowledge assistant for financial advisors

- IKEA: Deployed GenAI to summarise customer support logs and predict product return issues

- Unilever: Automates internal documents, policies, and supply chain emails using LLMs

GenAI for Knowledge Management

Enterprises are increasingly using GenAI for internal search, documentation, and knowledge retrieval. Examples include:

- Semantic search engines trained on internal wikis

- Retrieval-augmented generation (RAG) models surfacing real-time answers from live company data

- Secure GenAI interfaces trained on proprietary or regulated content

Risks and Limitations

- Hallucinations: LLMs can still invent facts in high-stakes domains (finance, healthcare)

- Latency & Cost: Running advanced LLMs at scale can be prohibitively expensive

- Data Privacy: Enterprises are cautious about data leaks via third-party model usage

- IP Clarity: Uncertainty remains on legal ownership of AI-generated outputs

Market Forecast

Generative AI alone is expected to drive $1.3 trillion in global economic impact annually by 2030, according to McKinsey Global Institute.

5. AI Jobs, Salaries & Workforce Impact

Artificial intelligence is reconfiguring the global labour market. It is not merely about job automation—it is about workforce transformation. In many sectors, AI is replacing repetitive tasks, while simultaneously giving rise to entirely new categories of jobs that didn’t exist five years ago.

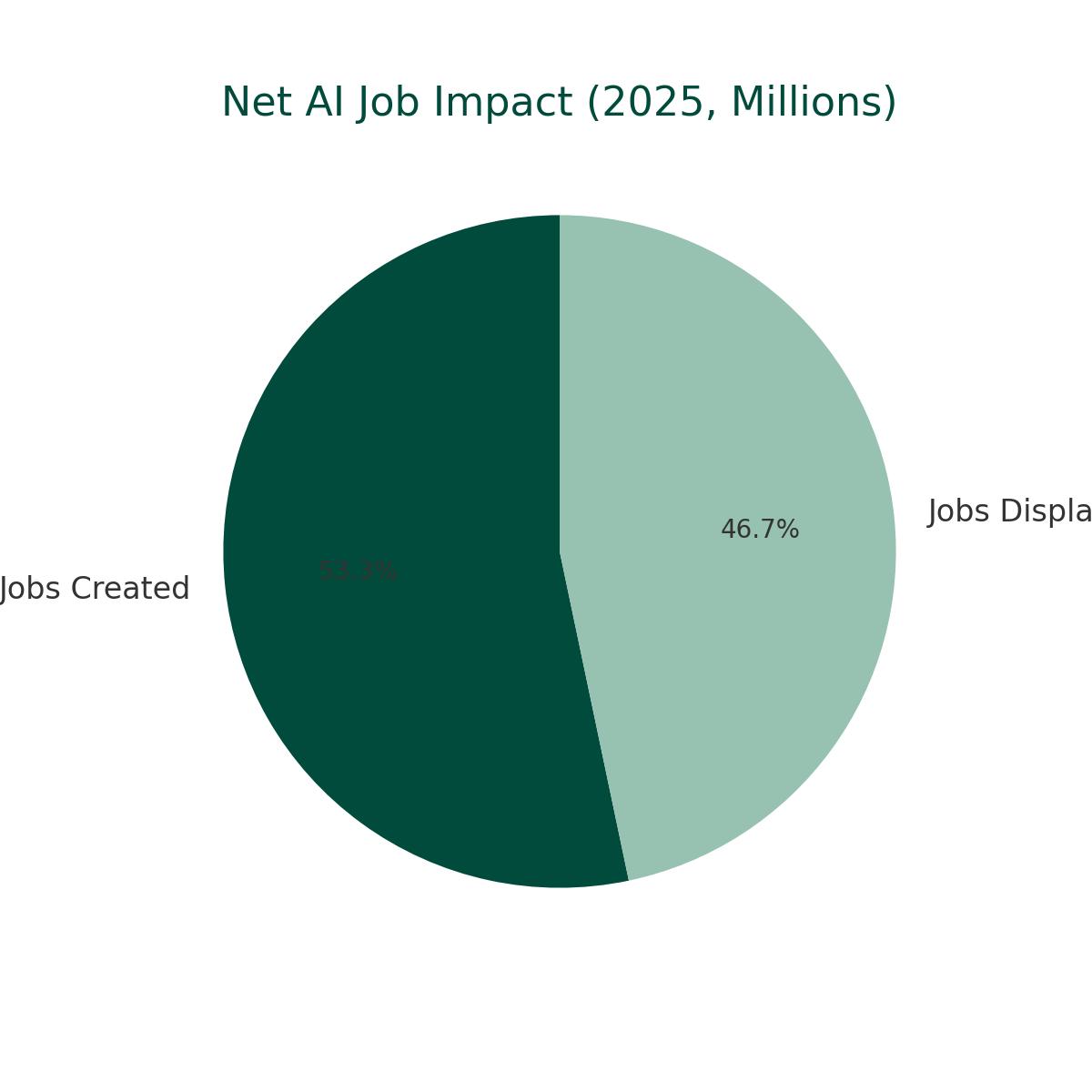

Net Impact

- 97 million jobs created globally due to AI (WEF forecast, 2025)

- 85 million jobs displaced (mostly repetitive, process-based roles)

- Net gain: +12 million, with significant variation across regions and skill levels

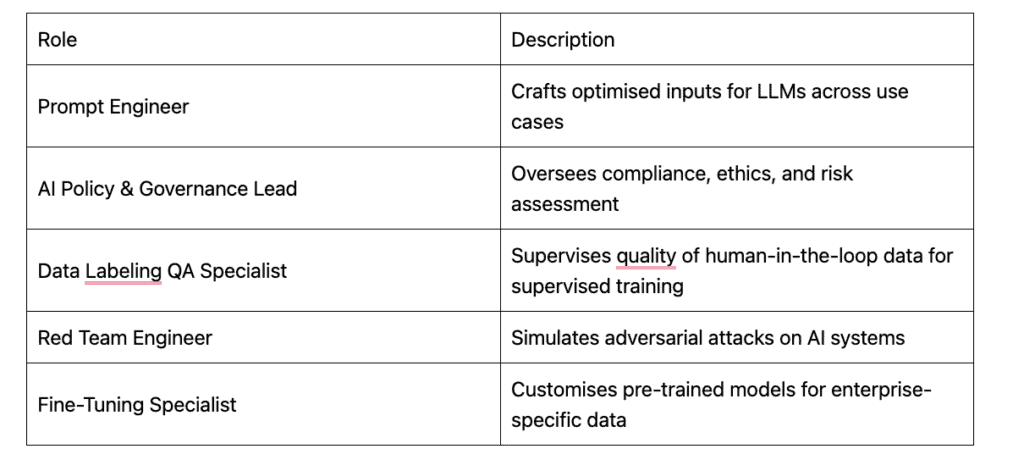

Top Roles Created by AI

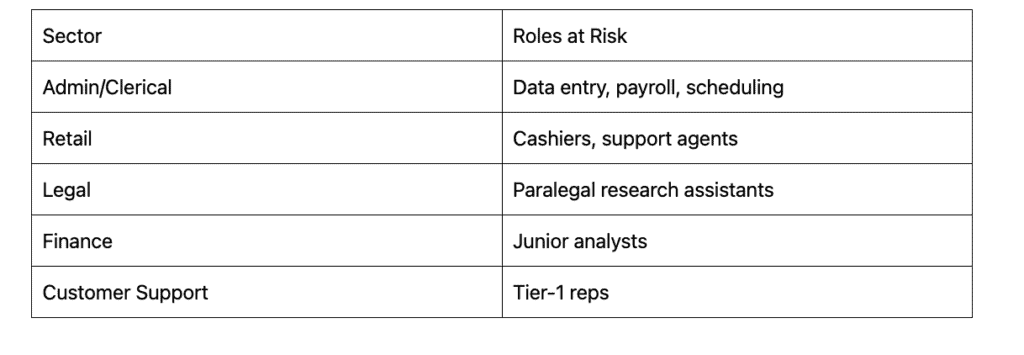

Roles Most at Risk

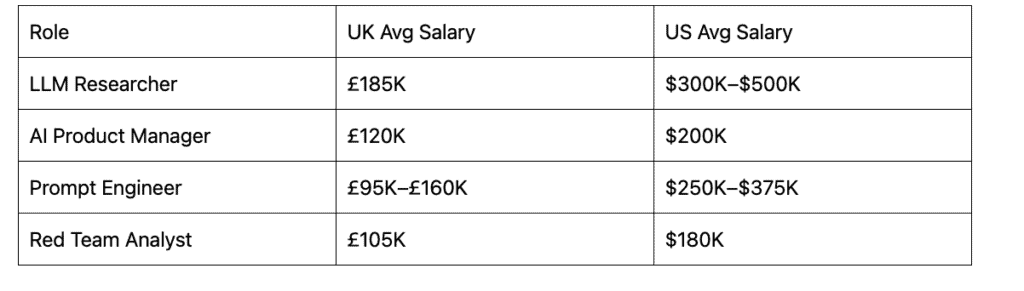

Global Salary Benchmarks (2025) (Source: ExplodingTopics)

Global Salary Benchmarks (2025) (Source: ExplodingTopics)

(Source: ExplodingTopics)

Upskilling and Education

Leading platforms for AI reskilling and certification include:

- Google Digital Garage (UK): Free GenAI courses for SMEs and students

- AWS AI Ready: 8 free AI and ML courses aimed at 2 million learners by 2026

- Coursera & DeepLearning.AI: Technical training in LLMs, RLHF, and neural networks

- Hugging Face Open Education: Hands-on, open-source training on NLP and Transformers

National Workforce Strategies

- UK: Skills for Life, AI Skills Lab, and DSIT-backed initiatives in AI bootcamps

- Singapore: AI Singapore (AISG) pairing SMEs with AI apprentices and engineers

- India: NASSCOM FutureSkills Prime—government-subsidised AI certifications

6. AI by Industry

AI is not a monolith—it is a multiplier. Different industries are experiencing varied levels of adoption and impact. Below is a sector-by-sector breakdown of how AI is being used and where it’s going next.

Healthcare

Current Applications:

- Early-stage diagnosis using computer vision (e.g. Skin Analytics)

- Remote triage with AI chatbots (e.g. Babylon Health)

- Predictive health monitoring using wearables + ML (e.g. Biofourmis)

Emerging Trends:

- Generative AI summarising EHR notes into discharge summaries

- LLMs translating medical documentation into plain English

- Synthetic trial simulation for faster drug approvals

Value Creation Forecast: $194B by 2030

Finance

Current Applications:

- AI-driven fraud detection (real-time transaction scanning)

- AI-enhanced underwriting and alternative credit scoring

- Sentiment-based trading models using LLMs on earnings calls

Emerging Trends:

- Autonomous wealth management assistants

- LLMs generating analyst reports on-demand

- Real-time ESG risk assessment via AI models

Notable Use: JPMorgan Chase has over 300 AI use cases in production, including fraud detection and generative tools for document processing.

Retail

Current Applications:

- AI-powered recommendation engines (e.g. Amazon Personalize)

- Dynamic pricing and demand forecasting

- Virtual fitting rooms and visual product search

Emerging Trends:

- AI for real-time customer segmentation

- Chat-driven ecommerce journeys using GenAI

- LLM-powered inventory and logistics orchestration

Manufacturing & Logistics

Current Applications:

- Predictive maintenance (AI detecting equipment failure in advance)

- Route optimisation and last-mile delivery forecasting

- Computer vision for assembly line QA

Emerging Trends:

- Robotics + AI integration for delicate tasks

- Digital twins with AI simulations to test factory flows

- Generative AI designing custom components

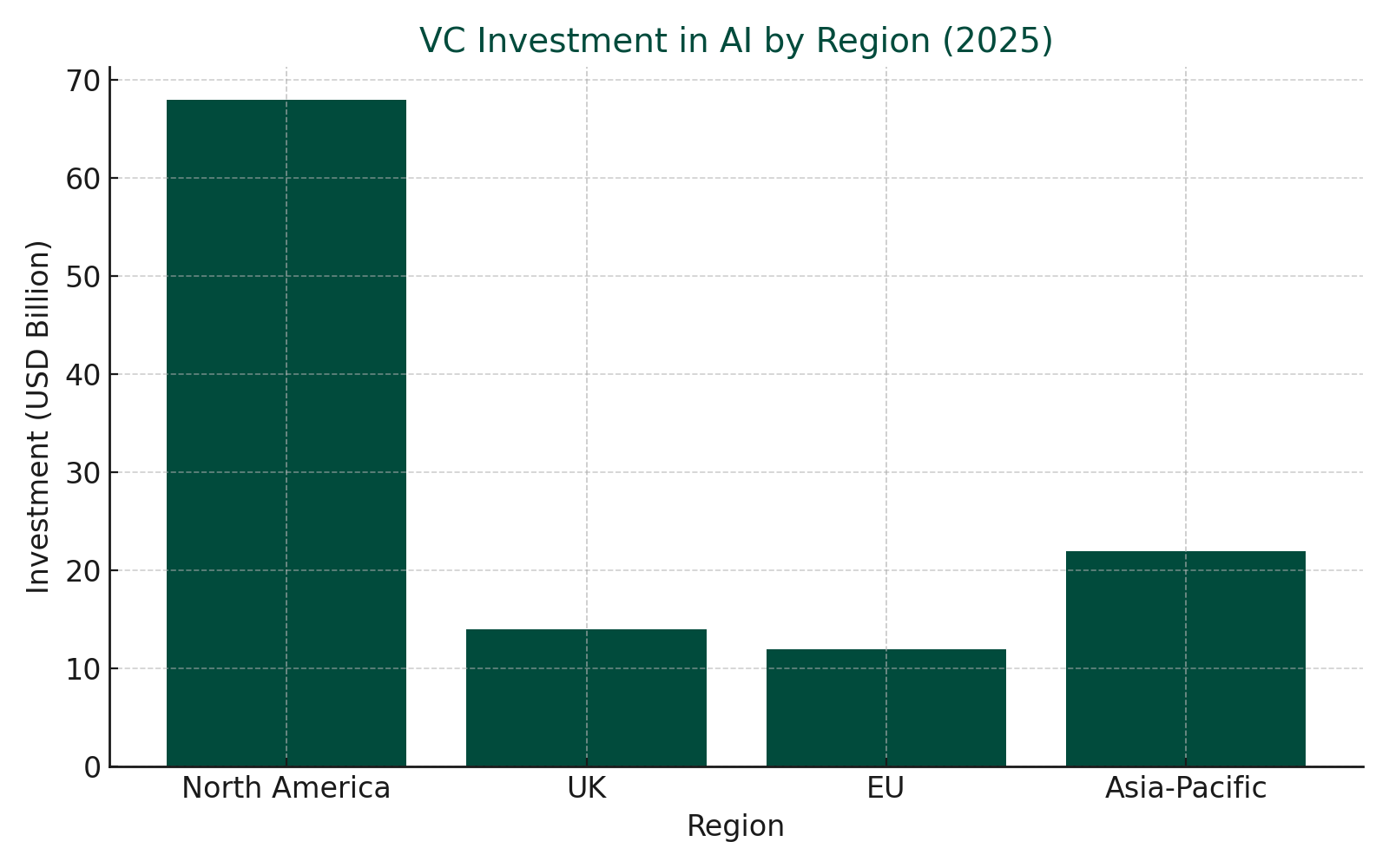

7. Investment in AI Startups

Investment in AI continues to outpace nearly every other tech vertical. In 2025, despite macroeconomic caution, AI startup funding has surged—driven by massive rounds in GenAI infrastructure, sector-specific applications, and sovereign AI models.

2025 Global Snapshot

- $107 billion deployed globally into AI startups (up 28% YoY)

- 5 of the 10 largest funding rounds of 2025 were in AI

- AI startups account for 26% of all global VC funding

UK in Focus

The UK remains Europe’s top destination for AI capital:

- Over £4.5B invested in 2024–2025

- Notable deals include Synthesia ($150M Series C), Quantexa ($180M), Stability AI (continued infrastructure rounds)

- London, Cambridge, and Edinburgh house the largest clusters, though Bristol and Oxford are growing

(Source: TechNation)

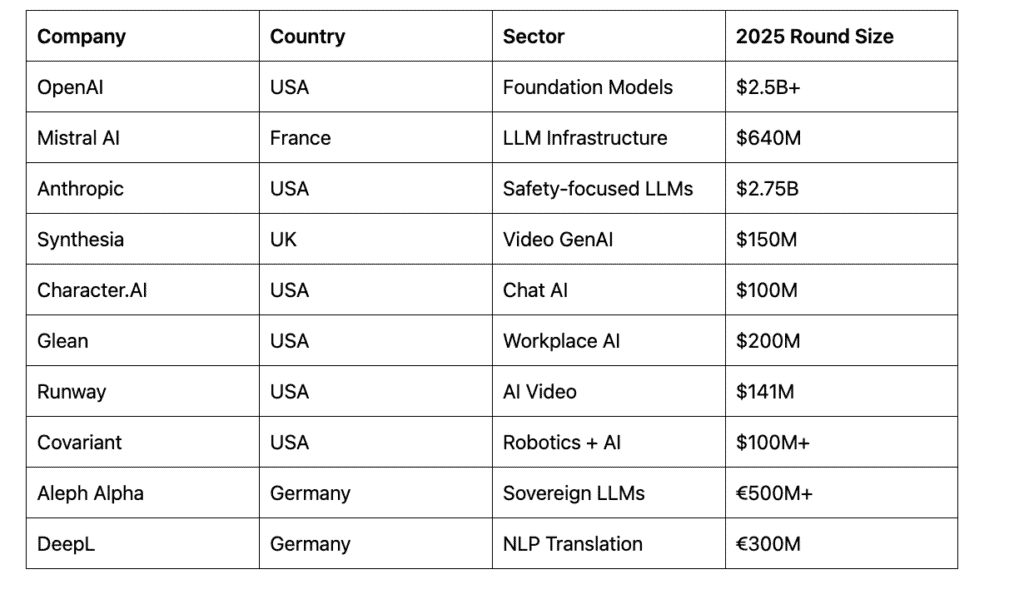

Top 10 Funded AI Startups (2025)

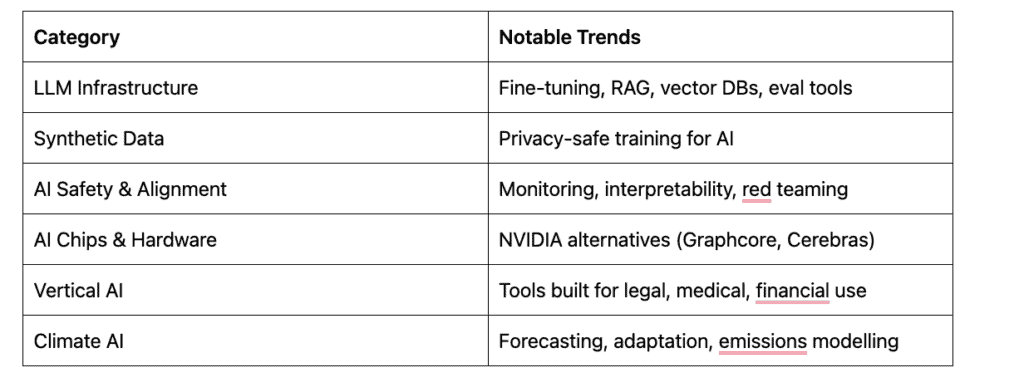

Investment Focus Areas

LP & Corporate Trends

- Sovereign wealth funds (e.g. UAE’s Mubadala) increasingly back GenAI scale-ups

- Corporate VCs like Salesforce Ventures, Intel Capital, and Google GV are active in vertical AI

- Family offices are funding early-stage AI for longevity, climate, and bioengineering

8. AI Regulation, Ethics & Risk

As AI becomes more powerful and more pervasive, the need for robust regulatory frameworks grows. Yet there is no global consensus—just a patchwork of national policies, voluntary standards, and emerging enforcement mechanisms.

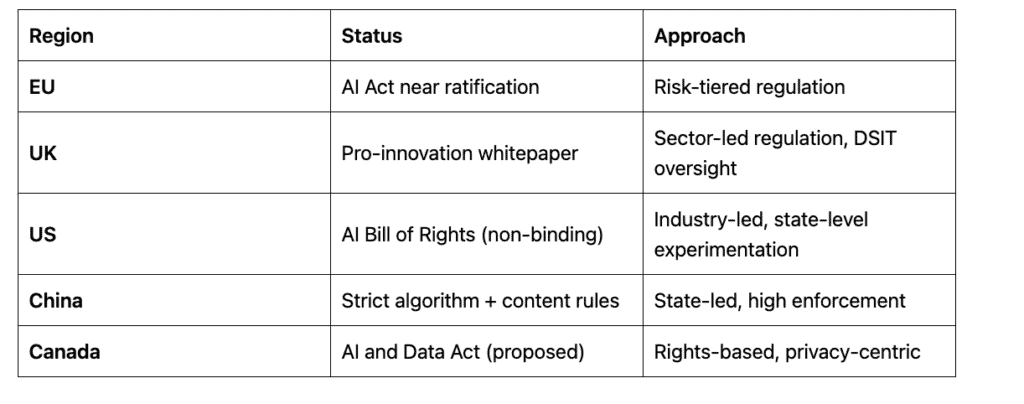

Regulation by Region

Key Policy Innovations

- UK Frontier AI Taskforce: Funded to assess national compute needs, safety testing, and open standards

- EU AI Act: Imposes obligations by application risk level—from banned (e.g. social scoring) to minimal oversight (e.g. spam filters)

- US Executive Order on AI (2023): Promotes model evaluations, watermarking, and workforce protections

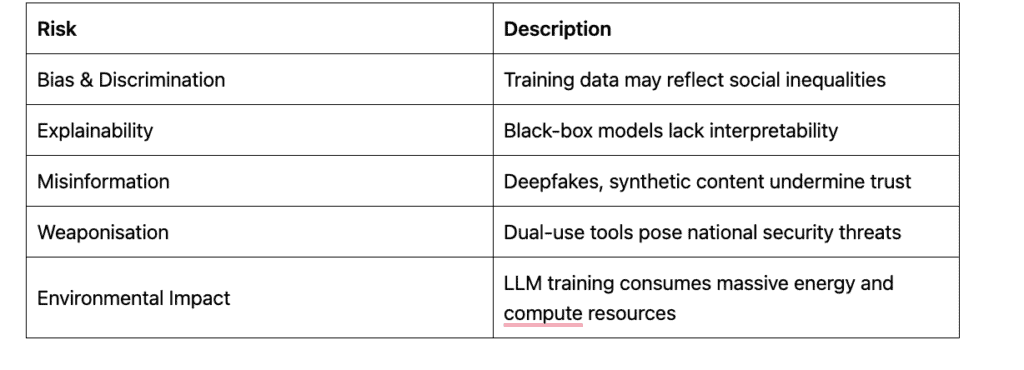

Major Risk Areas

Solutions Underway

- AI audits & model evals: Common at large firms, growing among startups

- Watermarking & provenance: OpenAI, Google, and Adobe launching detection standards

- Open model registries: Hugging Face and the UK Frontier Taskforce building transparency tools

The Path Forward

Effective regulation will likely depend on:

- International cooperation (e.g. G7’s Hiroshima AI Process)

- Compute registries and licensing regimes

- Increased funding for AI assurance startups and research

- Education and civic engagement to drive AI literacy

9. Future of AI: Predictions for 2025–2030

AI is not just evolving—it’s accelerating. As infrastructure matures, model capabilities improve, and capital flows in, the 2025–2030 period is set to redefine global competitiveness.

Key Global Predictions

- By 2026, over 95% of customer support interactions will involve AI

- By 2027, sovereign AI models will be launched in at least 25 countries

- By 2028, AI-generated scientific papers will outpace human-only authored papers in quantity

- By 2030, AI will contribute more than $15.7 trillion to global GDP (PwC)

Strategic Frontiers

- Sovereign AI Models: Nations building LLMs trained on local languages and values (e.g. Mistral, Aleph Alpha)

- Compute Nationalism: US, EU, and China racing to control chip manufacturing and access

- Bio + AI: Protein design, synthetic biology, personalised medicine

- AI + Robotics: Humanoid robotics (e.g. Figure, Tesla Bot) entering industrial and personal service

Cultural and Policy Shifts

- “AI Literacy” will become a mandatory part of national school curricula

- National compute infrastructures will be classified as critical infrastructure (like power or water)

- Private AI firms will face transparency mandates similar to public utilities

Final Thought

The AI revolution will not be televised, it will be embedded. From invisible APIs that rewrite supply chains to autonomous systems that co-create with humans, AI is shifting the base layer of how society functions.

10. Conclusion

Artificial Intelligence in 2025 is no longer a concept in the future tense. It is a defining force of the present—and one that is evolving faster than any prior technological revolution. What started as a narrow computational discipline has become a multi-trillion-dollar general-purpose technology, transforming how we work, live, govern, invest, and learn.

Across every major global region, AI is triggering economic value creation, labour market disruption, and infrastructure reimagination. It is not only shaping industries such as finance, healthcare, and logistics, but also forming the basis of new ones—such as AI safety, synthetic biology, and autonomous science.

Yet for all its promise, AI presents profound questions:

- Who builds it?

- Who controls it?

- Who benefits from it?

- And what happens if we get it wrong?

The urgency of these questions demands bold yet balanced action from every part of the global ecosystem—founders, governments, investors, researchers, and citizens.

For founders, this is the decade to build AI-native companies—startups that don’t just use AI as a feature, but as their foundation.

For governments, this is the moment to balance innovation with safety—to create policy that supports ambition without ignoring accountability.

For corporates, this is the time to scale beyond pilots—to rethink workflows, products, and even value chains around AI-driven insights.

For civil society, this is the opportunity to demand transparency, fairness, and inclusion—ensuring AI works for the many, not the few.

In many ways, 2025 marks the beginning of an AI-shaped society. The real question is not whether AI will change our world—it already has—but whether we will guide that change wisely, justly, and collectively.

11. References

This white paper draws on data and insights from the following public sources and research platforms. All insights have been reinterpreted, summarised, or reformulated to create original analytical content.

- Exploding Topics: AI Statistics 2024–2025

- Tech Nation: UK AI Sector Spotlight 2025

- Tech Nation: The UK’s Growth Potential Report 2025

- McKinsey Global Institute Reports (AI Adoption, GenAI Impact)

- PwC Global AI Economic Projections

- OECD AI Policy Observatory

- LinkedIn Economic Graph

- OpenAI, Anthropic, Meta, Hugging Face documentation

- AI Index 2024 (Stanford HAI)

- G7 Hiroshima AI Process Briefings

- UK Frontier AI Taskforce Strategy Paper (2024)

- European Commission AI Act Documentation